- Free Consultation: (772) 418-0949 Tap Here to Call Us

IRS Installment Agreement Strategy | Jacksonville IRS Help

IRS Installment Agreement Strategy: Jacksonville IRS Installment Agreement Help That Actually Works

If you are searching for Jacksonville IRS installment agreement help, there is a good chance you are dealing with an IRS balance due, collection notices, wage garnishments, bank levies, or increasing pressure from the IRS collection division.

Many taxpayers view an IRS installment agreement as nothing more than a payment plan. While that description is technically correct, it often misses the bigger picture.

An effective IRS Installment Agreement Strategy is not simply about obtaining approval from the IRS. It is about determining whether an installment agreement is the right solution, structuring the agreement in a sustainable manner, protecting your financial position, and integrating the agreement into an overall tax resolution strategy.

In many cases, the installment agreement itself is not the final objective. Instead, it may serve as a tool to stop aggressive IRS collection activity, preserve assets, maintain financial stability, or create time to pursue a more favorable long-term resolution.

Every taxpayer’s situation is different. A payment arrangement that makes sense for one taxpayer may be completely inappropriate for another. That is why I begin every case with an investigation rather than a predetermined solution. Providing correct resolution support to Jacksonville area taxpayers is the core mission of Harmon Tax Resolution.

Why My Background as a Tax Attorney, CPA, and Enrolled Agent Matters

IRS installment agreements sit at the intersection of tax law, financial analysis, and IRS procedure.

Many professionals approach IRS problems from only one perspective. Some focus primarily on legal issues. Others focus on accounting and financial analysis. Still others focus on navigating IRS procedures. Developing an effective IRS Installment Agreement Strategy often requires legal analysis, financial analysis, and a practical understanding of IRS procedures.

My background as a Tax Attorney, Certified Public Accountant (CPA), and IRS Enrolled Agent allows me to evaluate all three.

As a Tax Attorney, I analyze collection statutes, appeal rights, liens, levies, procedural issues, and the legal authority governing IRS collection actions. I am often looking beyond the immediate collection problem to understand how today’s decisions may affect the taxpayer years from now.

As a CPA, I analyze financial information. Installment agreements frequently rise or fall based upon income, expenses, asset equity, cash flow, future earning capacity, and the tax consequences associated with various financial decisions.

As an Enrolled Agent, I bring practical experience working within the IRS administrative system. This includes transcript analysis, Revenue Officer procedures, collection operations, and an understanding of how IRS personnel evaluate financial information.

Together, these perspectives allow me to evaluate the legal issues, financial issues, and procedural issues before recommending a resolution strategy. The goal is not simply obtaining an installment agreement. The goal is identifying the strategy that produces the best overall outcome for the taxpayer.

It is important to make sure to partner with a trustworthy, capable and reputable tax resolution firm who will ensure the best strategy is put forward.

What Most Taxpayers Get Wrong About IRS Installment Agreements

One of the most common misconceptions I encounter is the belief that every taxpayer who cannot immediately pay their tax debt should simply request a payment plan.

While installment agreements are often an excellent tool, that assumption can lead taxpayers down the wrong path.

I routinely encounter taxpayers who enter the wrong type of installment agreement, agree to unnecessarily high monthly payments, trigger avoidable financial disclosure requirements, overlook collection statute issues, and fail to consider other available resolution options.

The issue is not whether the IRS will approve an installment agreement.

The issue is whether the installment agreement makes sense when viewed in the context of the taxpayer’s entire financial and legal situation.

How an IRS Installment Agreement Strategy Begins With Investigation

Before recommending any installment agreement, I conduct a thorough investigation. Every IRS Installment Agreement Strategy should begin with a thorough investigation of the taxpayer’s facts and circumstances.

When evaluating an IRS collection case, I want to understand what the IRS believes is owed, how the liability arose, how long the IRS has to collect the debt, whether liens or levies exist, whether prior agreements have been established, whether compliance concerns exist, and whether other resolution options may produce a better overall result.

This process often begins with a review of IRS transcripts.

Transcripts can reveal information that taxpayers frequently do not realize exists, including prior collection actions, assessment dates, collection statute information, lien filings, installment agreement history, and pending collection activity.

I also review the taxpayer’s compliance history. A taxpayer who has previously defaulted an installment agreement may face different challenges than a taxpayer requesting a payment arrangement for the first time.

Most importantly, I am looking for opportunities.

I evaluate whether all allowable expenses have been properly considered, whether collection statutes have been correctly calculated, whether appeal rights remain available, and whether another resolution option may produce a more favorable result.

The investigation is not about forcing a particular solution. It is about identifying the best available solution.

IRS Financial Analysis: More Than Income and Expenses

The IRS generally evaluates a taxpayer’s ability to pay using standards found throughout IRM 5.14 (Installment Agreements) and IRM 5.15 (Financial Analysis Handbook).

The Internal Revenue Manual (IRM) is the primary operating manual used by IRS employees. While it is not the Internal Revenue Code, it provides important guidance regarding how IRS personnel evaluate collection cases.

The IRS frequently relies on National Standards and Local Standards when evaluating allowable living expenses. These standards establish guideline amounts for categories such as food, housing, transportation, and other necessary expenses.

However, these standards do not always tell the entire story.

In certain situations, taxpayers may have legitimate expenses that exceed standard allowances. The IRS may allow certain expenses above the National and Local Standards when the taxpayer can demonstrate that the expenses are necessary and reasonable under the circumstances. Examples may include:

- Extraordinary medical expenses

- Disability-related expenses

- Court-ordered obligations

- Special educational needs

- Other necessary expenses supported by documentation

Part of my analysis involves determining whether deviations from standard allowances are appropriate and whether sufficient documentation exists to support those deviations.

The difference between a sustainable installment agreement and an unsustainable installment agreement is often not income. It is whether the financial analysis was performed correctly.

Evaluating Assets, Equity, and Borrowing Potential

Another important part of the analysis involves taxpayer assets and available equity.

Many taxpayers assume that simply because they own a home, retirement account, business interest, or investment asset, the IRS will automatically require liquidation before considering an installment agreement.

Conversely, some taxpayers assume that the IRS will ignore those assets entirely.

Neither assumption is always correct.

As part of its financial analysis, the IRS may evaluate whether equity exists in certain assets and whether that equity is reasonably available to satisfy the liability. The IRS may also consider whether borrowing against assets is possible.

However, the existence of equity does not automatically mean liquidation is the appropriate solution.

Factors such as age, health, retirement status, marketability, borrowing ability, cash flow, tax consequences, and overall economic reality may all affect the analysis.

The IRS may also evaluate whether a taxpayer has the ability to borrow against assets rather than liquidate them outright.

For example, the IRS may consider whether equity exists in a personal residence, retirement account, investment account, business asset, or other property that could potentially be used to satisfy the tax liability.

However, the existence of equity does not automatically mean borrowing is realistic, available, or appropriate.

In evaluating borrowing potential, I frequently examine factors such as:

- The taxpayer’s age and retirement status

- Existing debt obligations

- Creditworthiness

- Debt-to-income ratios

- Health concerns

- Lending restrictions

- Tax consequences associated with liquidation or borrowing

- Overall economic reality

In some cases, borrowing against an asset may be a reasonable solution. In other cases, forcing a taxpayer to borrow or liquidate assets may create more financial harm than benefit. A proper analysis requires far more than simply identifying available equity.

This is another reason why a complete investigation should occur before selecting a resolution strategy.

Real-World Example: Why Investigation Matters

One recent matter illustrates why a thorough investigation is critical before recommending an installment agreement.

The taxpayer owed approximately $180,000 to the IRS and earned a substantial annual income. At first glance, many practitioners would have assumed the taxpayer should liquidate assets or borrow against available resources to pay the liability.

However, a deeper investigation revealed a more complicated picture.

The taxpayer’s financial condition included retirement assets, ongoing financial obligations, future retirement concerns, and collection statute considerations that significantly impacted the analysis. Simply looking at the balance due and asset values did not tell the entire story.

After reviewing IRS transcripts, analyzing the Collection Statute Expiration Dates, evaluating the taxpayer’s cash flow, and examining the practical realities of the taxpayer’s financial situation, a structured installment agreement strategy was developed that protected the taxpayer’s long-term financial interests while resolving the IRS collection problem.

The lesson is simple. Effective IRS representation is rarely about finding the quickest solution. It is about finding the solution that produces the best overall outcome after considering all relevant facts and circumstances.

Types of IRS Installment Agreements

Streamlined Installment Agreements

Streamlined Installment Agreements are generally available for qualifying taxpayers with balances within IRS thresholds and typically do not require extensive financial disclosure.

These agreements are often the simplest option but are not always the best option.

Non-Streamlined Installment Agreements

When larger balances exist, the IRS may require detailed financial disclosures before approving a payment arrangement.

These cases often involve more extensive financial analysis and negotiation.

Partial Pay Installment Agreements

A Partial Pay Installment Agreement (PPIA) allows taxpayers to make monthly payments that may not fully satisfy the liability before the collection statute expires.

PPIAs are frequently overlooked but can be powerful tools when supported by the facts and circumstances of the case.

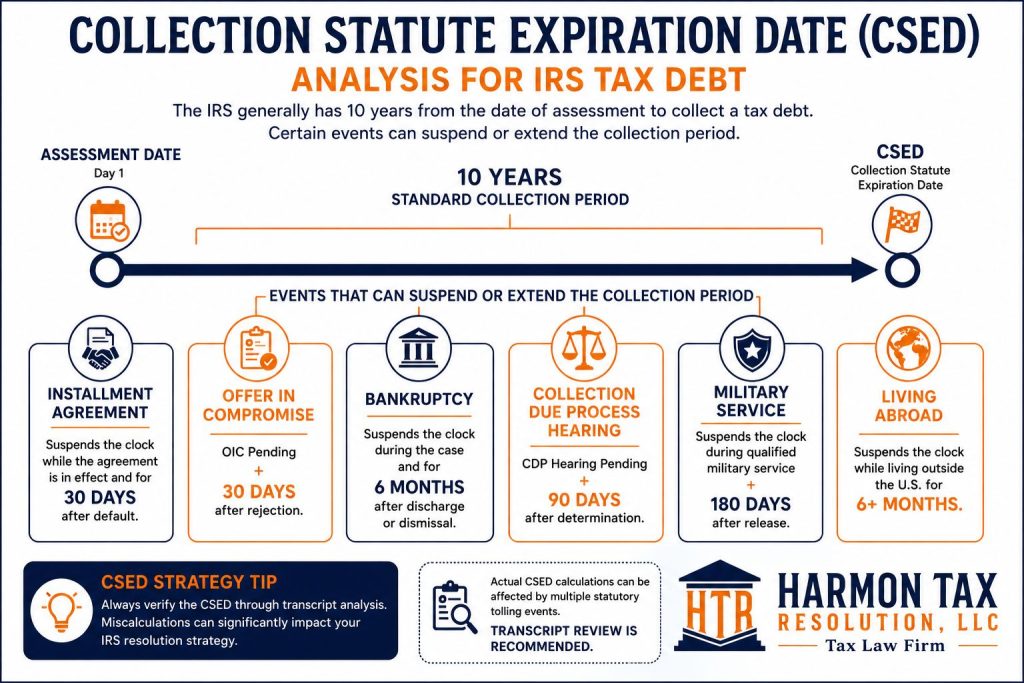

Understanding the Collection Statute Expiration Date (CSED)

The Collection Statute Expiration Date is often one of the most important factors when developing an IRS Installment Agreement Strategy.

Under IRC §6502, the IRS generally has ten years from assessment to collect a tax liability.

However, determining the actual expiration date is not always straightforward.

Certain events may suspend or extend the collection period, including:

- Bankruptcy proceedings

- Collection Due Process hearings

- Pending Offers in Compromise

- Certain military service periods

- Other statutory tolling events

This is one reason I never assume a collection statute calculation is correct without verification.

I have encountered situations where transcript analysis revealed issues that materially changed the strategy and outcome of a case.

When substantial time remains on the collection statute, one strategy may be appropriate. When only a limited amount of time remains, an entirely different strategy may produce a better result.

Collection Statute Expiration Date analysis can significantly impact installment agreement strategy and other IRS resolution options.

How an IRS Installment Agreement Strategy Can Stop IRS Collections

Internal Revenue Code §6159 authorizes the IRS to enter into installment agreements when doing so facilitates collection of a tax liability.

One of the most important benefits of a properly structured installment agreement is the protection it may provide against aggressive collection activity.

Depending on the status of the case, installment agreements may help prevent:

- Bank levies

- Wage garnishments

- Continued collection enforcement

- Additional collection pressure

Timing matters. The stage of the collection case matters. Whether a Revenue Officer has been assigned matters.

However, a properly structured installment agreement can often provide the breathing room necessary to stabilize a taxpayer’s financial situation and pursue a longer-term strategy.

Revenue Officer Cases Often Require a Different Strategy

Not all IRS collection cases are handled the same way.

Some cases remain within the IRS Automated Collection System (ACS), while others are assigned to a local Revenue Officer.

When a Revenue Officer becomes involved, the stakes often increase significantly.

Revenue Officers typically conduct more detailed investigations, request additional financial information, evaluate asset equity more aggressively, and have greater flexibility in pursuing enforced collection actions.

A Revenue Officer may request:

- Financial statements

- Bank records

- Proof of expenses

- Asset documentation

- Borrowing information

- Business records

The timing of collection actions may also accelerate.

Because Revenue Officers have greater discretion and direct involvement in the case, installment agreement strategy often becomes even more important. Financial disclosures must be carefully reviewed, collection statutes must be evaluated, and all available resolution options should be considered before submitting information to the IRS.

The approach that works in an Automated Collection System case may not be sufficient in a Revenue Officer case.

Understanding the difference can have a substantial impact on the outcome.

Compliance: The Foundation of Every Successful Installment Agreement

Obtaining approval is often the easy part.

Maintaining the agreement is where many taxpayers encounter problems.

The IRS generally requires taxpayers to remain compliant throughout the duration of the agreement.

This means:

- Filing future tax returns on time

- Paying future taxes as they become due

- Maintaining adequate withholding

- Making required estimated tax payments

One of the most common reasons installment agreements fail is pyramiding tax debt.

Pyramiding occurs when a taxpayer enters an agreement to resolve old tax liabilities while simultaneously creating new tax liabilities.

Before recommending an installment agreement, I evaluate whether the taxpayer can realistically remain compliant moving forward.

A payment arrangement that resolves prior tax debt but creates future tax problems is rarely a successful outcome.

Sometimes an Installment Agreement Is the Wrong Answer

Not every taxpayer should enter into an installment agreement.

Sometimes another resolution option may produce a better result.

Depending upon the circumstances, alternatives may include:

- Offer in Compromise

- Currently Not Collectible Status

- Innocent Spouse Relief

- Appeals

- Audit Reconsideration

The key is understanding the taxpayer’s complete financial and procedural situation before selecting a strategy.

An Installment Agreement Can Be a Bridge to a Better Resolution

Many taxpayers assume an installment agreement is the final resolution of their IRS problem.

In some cases, that is true.

In other cases, the installment agreement serves as a bridge to a more favorable long-term resolution.

For example, a taxpayer may need time for:

- Retirement

- Income changes

- Business restructuring

- Medical developments

- Expiration of collection statutes

- Additional documentation development

A properly structured installment agreement can provide stability and protection while those opportunities develop.

Frequently Asked Questions About IRS Installment Agreements

How Long Can an IRS Installment Agreement Last?

The answer depends on the type of installment agreement, the amount owed, and the taxpayer’s financial circumstances.

Many taxpayers are familiar with Streamlined Installment Agreements, which often allow qualifying taxpayers to spread payments over as many as 72 months. However, that is not the only type of agreement available.

In some situations, the IRS may require a shorter repayment period based upon the taxpayer’s ability to pay. In other situations, a Partial Pay Installment Agreement may be appropriate when the taxpayer is unlikely to fully satisfy the liability before the Collection Statute Expiration Date (CSED).

The length of an installment agreement should not be determined solely by what produces the lowest payment. The agreement should be evaluated in light of the taxpayer’s financial condition, collection exposure, compliance requirements, and long-term resolution strategy.

Can the IRS Reject an Installment Agreement?

Yes.

Many taxpayers assume that if they offer a monthly payment, the IRS must accept it. That is not always the case.

The IRS evaluates installment agreement requests based upon the taxpayer’s compliance history, financial condition, ability to pay, and the specific type of agreement being requested.

For example, a taxpayer who has unfiled tax returns will generally need to become compliant before an agreement can be approved. Likewise, taxpayers who have defaulted previous agreements may face additional scrutiny.

The IRS may also reject a proposal if it determines the taxpayer has the ability to make larger payments or if required financial information is incomplete.

This is one reason I conduct a detailed investigation before submitting a proposal. Understanding how the IRS is likely to evaluate the case often allows problems to be addressed before they become obstacles.

Does an IRS Installment Agreement Stop Wage Garnishment?

In many situations, yes.

One of the primary benefits of a properly structured installment agreement is the protection it may provide from aggressive collection activity.

Depending upon the stage of the collection process, an approved installment agreement may prevent wage garnishments, bank levies, and other enforced collection actions.

In many cases, collection protections begin once a qualifying installment agreement request becomes pending. However, the exact impact depends upon the facts of the case, the status of the collection action, and whether a Revenue Officer has been assigned.

Because timing can be critical, taxpayers facing wage garnishment or levy action should generally seek assistance before collection activity progresses further.

What Is a Partial Pay Installment Agreement?

A Partial Pay Installment Agreement, commonly referred to as a PPIA, is a type of installment agreement in which the taxpayer makes monthly payments even though the liability may not be fully paid before the collection statute expires.

Unlike traditional installment agreements, the objective is not necessarily to pay the entire balance. Instead, the IRS evaluates the taxpayer’s ability to pay and may accept payments based upon current financial circumstances.

PPIAs can be particularly valuable when a taxpayer has limited disposable income and relatively little time remaining on the Collection Statute Expiration Date.

However, they are not appropriate in every situation. Careful financial analysis and statute review are critical before pursuing this strategy.

Can the IRS File a Tax Lien While I Am on a Payment Plan?

Possibly.

Many taxpayers incorrectly believe that entering into an installment agreement automatically prevents the IRS from filing a Notice of Federal Tax Lien.

The reality is more complicated.

Whether the IRS files a lien may depend on factors such as the amount owed, the type of installment agreement, the taxpayer’s collection history, and current IRS policies.

In some situations, strategic planning before entering into an agreement may reduce lien exposure. In other situations, a lien may be unavoidable regardless of the payment arrangement selected.

Because liens can affect financing opportunities, credit relationships, and asset transactions, this issue should be evaluated as part of the overall resolution strategy.

What Happens If I Miss a Payment?

Missing a payment does not always result in immediate termination of the agreement, but it can create significant problems.

Installment agreements generally require taxpayers to make all payments on time and remain compliant with future tax obligations.

If a taxpayer falls behind, the IRS may issue default notices and provide an opportunity to correct the problem. However, continued noncompliance may result in termination of the agreement and renewed collection activity.

In addition to missed payments, installment agreements frequently default because taxpayers fail to file future tax returns or incur additional tax liabilities.

For that reason, maintaining compliance is just as important as obtaining the agreement in the first place. If you miss a payment, make sure to make the next payment on time.

How Does the IRS Determine Monthly Installment Agreement Payments?

The IRS generally begins by evaluating the taxpayer’s financial condition.

This analysis often includes income, living expenses, assets, liabilities, and future earning potential.

IRS personnel frequently rely on financial guidelines found in the Internal Revenue Manual, including National Standards and Local Standards for certain categories of living expenses.

However, many taxpayers are surprised to learn that those standards do not always represent the final answer.

In appropriate circumstances, taxpayers may be able to justify expenses that exceed standard allowances. Medical conditions, disability-related costs, court-ordered obligations, and other documented circumstances may affect the analysis.

This is one reason detailed financial investigation can have a substantial impact on the outcome of a case.

Should I Choose an Installment Agreement or an Offer in Compromise?

There is no universal answer.

An Offer in Compromise and an Installment Agreement are different tools designed for different situations.

Some taxpayers are strong Offer in Compromise candidates because their assets and future income indicate that the IRS is unlikely to collect the full liability.

Others may not qualify for an Offer in Compromise but may still obtain an affordable installment agreement that achieves a favorable outcome.

There are also situations where a taxpayer may begin with an installment agreement and later pursue a different resolution strategy as circumstances change.

The correct choice depends upon the taxpayer’s income, assets, collection statute considerations, compliance history, and overall financial condition.

That is why I evaluate all available options before recommending a particular course of action.

Why Should I Hire a Tax Attorney, CPA, and Enrolled Agent for an IRS Installment Agreement?

Many installment agreement cases involve more than simply completing IRS forms.

A successful resolution often requires legal analysis, financial analysis, transcript review, collection statute evaluation, and a practical understanding of IRS procedures.

As a Tax Attorney, CPA, and Enrolled Agent, I evaluate each case from multiple perspectives. This allows me to analyze legal issues, financial issues, and procedural issues before recommending a strategy.

Rather than focusing solely on obtaining approval, my objective is to identify the resolution option that produces the best overall outcome based upon the taxpayer’s specific facts and circumstances.

Final Thoughts

A properly developed IRS Installment Agreement Strategy can be one of the most effective tools available to taxpayers facing IRS collections.

However, an installment agreement should never be viewed as merely a payment plan.

The IRS is not simply evaluating whether a taxpayer can make a monthly payment. The IRS is evaluating the taxpayer’s overall financial condition, ability to pay, asset equity, compliance history, and future collection potential.

A successful strategy requires more than completing forms and requesting approval.

It requires investigation.

It requires transcript analysis.

It requires financial analysis.

It requires an understanding of IRS procedures, collection statutes, and available resolution alternatives.

Most importantly, it requires selecting the solution that best fits the taxpayer’s unique facts and circumstances.

In some cases, that solution will be a streamlined installment agreement. In other cases, it may be a Partial Pay Installment Agreement, an Offer in Compromise, Currently Not Collectible status, or another resolution path entirely.

The objective is not simply obtaining an installment agreement.

The objective is achieving the best overall outcome.

Every IRS installment agreement strategy should begin with transcript analysis, financial review, and evaluation of all available resolution options.

Take Back Control of Your IRS Situation

If you are dealing with IRS debt, the worst thing you can do is wait or approach the IRS without a clear strategy.

An installment agreement, when structured properly, can:

• Stop IRS collections

• Protect your assets

• Give you a clear path forward

• Help you regain peace of mind

At Harmon Tax Resolution, LLC, we take a strategic approach to every case—because no two IRS situations are the same.

You may qualify for a solution that reduces your financial burden and helps you move forward with confidence. Contact Harmon Tax Resolution.

📞 Harmon Tax Resolution, LLC

Jacksonville: 904-616-8256

Port Saint Lucie: 772-418-0949

Clearwater: 813-325-6009

🌐 www.harmontaxresolution.com

Our Offices

Port St. Lucie, FL 34953

Clearwater, FL 33767

Ste#800

Jacksonville, FL 32207