- Free Consultation: (772) 418-0949 Tap Here to Call Us

IRS Offer in Compromise Strategy: What It Really Takes

Understanding the right IRS Offer in Compromise strategy can mean the difference between continued IRS pressure and finally resolving your tax debt the right way.

Most people don’t come to me when things are calm.

They come when the notices have piled up, the pressure is building, and they’re not sure what the IRS is going to do next.

If that sounds familiar, you’re not alone—and more importantly, you’re not out of options. If you’re reading this, there’s a good chance you’re trying to figure out what your next move should be before the IRS makes one for you.

There is a moment in almost every initial conversation where a taxpayer will say something like:

“I heard I can settle this for pennies on the dollar… do I qualify?”

It’s an understandable question.

But it usually comes from a place of urgency, stress, and incomplete information about how the IRS actually operates.

Because an Offer in Compromise is not a program you simply apply for.

It is not a discount the IRS offers because a situation feels difficult or overwhelming.

And it is certainly not something that can be accurately determined from a short conversation based on rough income and expense estimates.

An Offer in Compromise is a legal resolution mechanism under Internal Revenue Code §7122, and in real-world application, it is governed by the IRS’s internal framework—primarily Internal Revenue Manual (IRM 5.8)—which dictates how offers are reviewed, challenged, and ultimately accepted or rejected. The difference between acceptance and rejection often comes down to how well the case is developed, documented, and presented within those rules.

👉 The IRS is not negotiating based on sympathy

👉 The IRS is calculating based on collectibility

They are asking one central question:

👉 “What is the most we can reasonably collect from this taxpayer over time?”

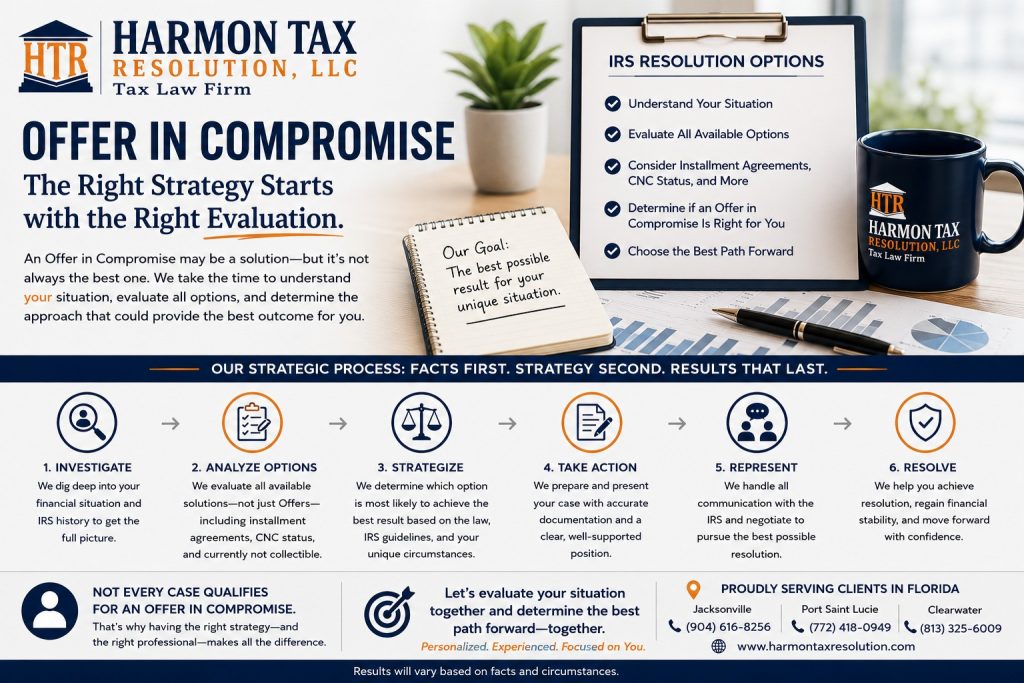

What Is an IRS Offer in Compromise Strategy

An IRS Offer in Compromise strategy is not simply submitting a form to reduce tax debt. It is a structured, multi-layered approach that evaluates your financial condition, IRS collection posture, and legal positioning before any resolution is pursued.

A proper strategy looks at:

- Your ability to pay based on real financial data, not assumptions

- IRS enforcement risk, including levies and garnishments

- The timing of your case within the IRS collection process

- Whether alternative solutions like IRS installment agreement options may actually produce a better outcome

👉 Without strategy, an Offer is just a guess. And guessing is exactly what leads to rejected offers, wasted time, and continued IRS pressure.

🔍 Before There Is an Offer, There Is an Investigation

When I take on a case, I am not thinking about forms.

I am not thinking about submission timelines.

I am thinking:

👉 What is actually happening here, and how will the IRS interpret it?

Because until that is fully understood, any attempt at resolution is premature.

How IRS Offer in Compromise Strategy Actually Works

Where the Taxpayer Sits in the IRS Collection Process

A taxpayer’s position within the IRS collection system directly impacts available options, urgency levels, and overall strategic approach, especially when determining whether immediate action or structured planning is required.

A newly assessed liability generally allows more flexibility, planning time, and opportunity to develop a favorable financial position before IRS scrutiny intensifies and enforcement risk escalates significantly.

A case that has progressed into active collections introduces pressure, tighter timelines, and increased likelihood of enforced collection actions such as levies or wage garnishments being initiated by the IRS.

A taxpayer who has received a Final Notice of Intent to Levy (LT11) is now facing imminent enforcement, requiring immediate intervention to prevent wage garnishment, bank levies, or seizure of assets.

A liability approaching the Collection Statute Expiration Date under IRC §6502 may shift strategy entirely toward preserving time and avoiding actions that unnecessarily extend the collection period.

👉 This positioning determines whether you act immediately, strategically delay, or build before presenting.

Whether Enforcement Action Is Imminent or Already Underway

The presence or absence of enforcement activity significantly changes how a case must be handled from the outset and what tools must be deployed to protect the taxpayer.

If the IRS is preparing to levy wages or bank accounts, the situation requires immediate defensive action to prevent financial disruption, protect income streams, and maintain control over daily financial obligations.

If enforcement has not yet begun, there may be an opportunity to proactively structure the case, strengthen financial positioning, and prepare a defensible resolution before the IRS escalates collection efforts.

A Final Notice of Intent to Levy triggers rights under IRC §6330, allowing the taxpayer to request a Collection Due Process hearing within strict time limits.

A properly filed CDP hearing halts enforcement activity, transfers the case to Appeals, preserves the taxpayer’s right to petition Tax Court, and creates time to properly evaluate and build a resolution strategy.

👉 If you are facing enforcement, understanding how to stop an IRS levy becomes critical before submitting any resolution.

How the Liability Is Structured Across Tax Years

Each tax year carries its own legal status, assessment timeline, and collection characteristics that must be evaluated independently rather than treated as a single combined liability.

Some tax years may be nearing expiration under the collection statute, making aggressive resolution unnecessary or even harmful if it extends the statute unnecessarily.

Other years may be recently assessed, fully collectible, and subject to immediate enforcement if not addressed properly.

Certain liabilities may contain errors, misapplied payments, or incorrect assessments that could significantly alter the overall case outcome if identified and corrected early.

👉 A proper strategy isolates each year and applies the correct resolution logic individually.

What the Actual Collection Statutes Are—and Whether They Are Correct

The IRS operates under a general 10-year collection statute under IRC §6502, but that timeline is frequently altered by tolling events and administrative actions that extend or suspend the period.

It is not uncommon for IRS records to reflect statute dates that require independent verification, especially in cases involving prior installment agreements, bankruptcy filings, offers in compromise, or CDP hearings.

Failure to verify these dates independently can result in pursuing unnecessary resolution options, extending collection periods, or missing opportunities where the liability may already be unenforceable.

👉 Verifying the statute is not optional—it is a critical component of strategy.

How Income Flows in Reality—Not Just on a Tax Return

The IRS evaluates income based on actual financial activity, not solely what is reported on filed tax returns or what the taxpayer believes represents their income.

Bank deposits, inter-account transfers, third-party reporting documents, and overall cash flow patterns are used by the IRS to reconstruct income where discrepancies exist.

If reported income does not align with actual deposits or lifestyle indicators, the IRS will adjust income figures during the review process to reflect what they determine to be accurate.

👉 If the financial picture is unclear, the IRS will create one that is not in your favor.

👉 Struggling with IRS debt or facing a levy? You may qualify for relief—but only with the right IRS Offer in Compromise strategy. Schedule a consultation today and take control before the IRS does.

🔥 What’s Really Involved in an Offer in Compromise

🔥 Real Case Studies: How This Works in Practice

Now that you understand how an IRS Offer in Compromise strategy actually works on paper, let’s look at what happens in real life—because this is where most of the real work takes place.

This is how real cases unfold.

And what most people never see is this:

👉 The result is the smallest part of the story

👉 The real work is everything that leads up to it

These are not “submit and hope” cases.

They are built, tested, adjusted, defended, and carried across the finish line.

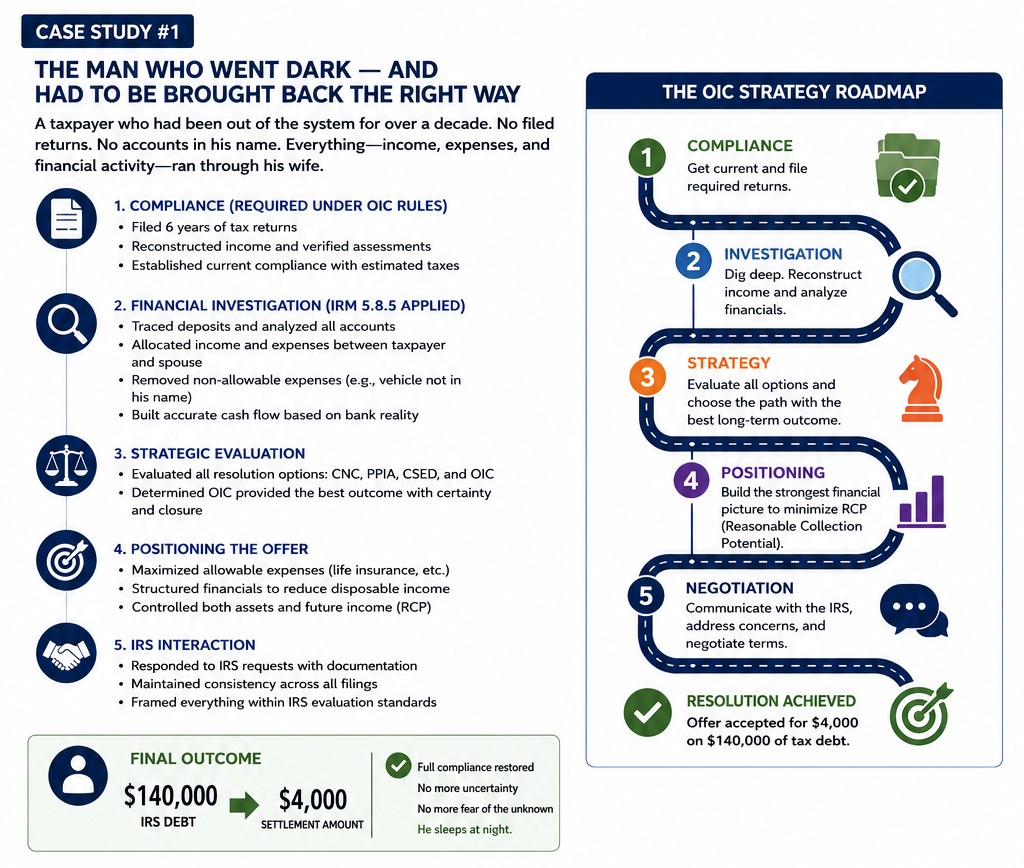

💥 Case Study #1: The Man Who Went Dark — And Had to Be Brought Back the Right Way

When my client first came to me, this was not a typical tax case.

This was a situation where someone had effectively stepped outside the system for over a decade.

No filed returns.

No accounts in his name.

No assets in his name.

Everything—income, expenses, and financial activity—ran through his wife.

😰 What It Felt Like to Be Him

He wasn’t ignoring the problem because he didn’t care.

He was stuck because he didn’t know:

👉 How far this had gone

👉 What the IRS could actually do

👉 Whether stepping forward would make things worse

That uncertainty builds over time.

And when you’ve been out of the system that long, the fear isn’t just the debt…

👉 it’s the unknown consequences of stepping back into the system

🔍 What I Saw Immediately (Applying IRS Reality — Not Assumptions)

This wasn’t a “no asset” case.

This was a financial reconstruction case under IRM 5.8.5 (Financial Analysis).

Because under IRS rules:

👉 The IRS does NOT care whose name the account is in

👉 They care where the money flows and who benefits

And if that is not clearly explained and documented, the IRS will make its own determination—and it is almost never in the taxpayer’s favor.

So immediately I identified:

- Exposure to bank deposit analysis (indirect income method)

- Need to establish economic reality vs legal title

- Risk of IRS attributing 100% of deposits to taxpayer if not clarified

🧠 Phase 1 — Compliance (Required Under OIC Rules)

Before an Offer is even considered under IRC §7122 and IRM 5.8.3, the taxpayer must be compliant.

That meant:

- Filing the last six years of returns (IRM compliance requirement – IRM 1.2.1.6.18 – Policy Statement 5-133)

- Accurately reconstructing income (not estimates)

- Establishing current compliance with estimated tax payments

- Monitoring transcripts to confirm assessments and balances

👉 If this step is wrong, the IRS rejects the Offer before review

This is where my background matters:

👉 This wasn’t just tax prep — this was building a defensible position the IRS would accept

🔬 Phase 2 — Financial Investigation (IRM 5.8.5 Applied Line-by-Line)

This is where most “mills” fail.

We didn’t just fill out a 433-A (OIC).

We:

- Traced deposits into spouse’s accounts

- Built allocation schedules to separate income streams

- Identified what was actually his vs household

- Reconstructed cash flow based on bank reality, not assumptions

- Removed items that would be disallowed under IRS allowable expense rules (IRM 5.15)

👉 Example:

The vehicle had to be removed because:

- It was not in his name

- He could not substantiate ownership or payment responsibility

- IRS would disallow under asset/expense verification rules

🔁 Iteration Process (Critical Under IRS Scrutiny)

This did NOT happen in one pass.

We:

- Built the financials

- Challenged them

- Asked follow-up questions

- Rebuilt them again

👉 Multiple times

Why?

Because under IRM review:

👉 Inconsistency = rejection risk

We made sure:

- Income matched deposits

- Expenses matched documentation

- Allocations made sense logically

⚖️ Phase 3 — Strategic Evaluation (Not Just “Do an OIC”)

We evaluated ALL options:

- CNC (IRC §6343) → hardship positioning

- PPIA (IRC §6159) → partial pay over time

- CSED strategy (IRC §6502) → timing analysis

There were real scenarios where:

👉 letting the statute run could have worked

But that lacked:

- certainty

- closure

- control

So we moved forward with strategy — not default

🔧 Phase 4 — Positioning the Offer (THIS is where the case was won)

We didn’t just submit numbers.

We engineered the outcome within IRS rules:

- Identified allowable expenses not being used

- Introduced legitimate expenses (life insurance — allowable under IRM when justified)

- Structured financials to reduce disposable income under RCP calculation rules

👉 RCP = Assets + Future Income (IRM 5.8.5)

We controlled BOTH sides.

🏛 Phase 5 — IRS Interaction (Speaking Their Language)

This is where most cases fall apart.

But I understand:

👉 how examiners evaluate

👉 what triggers pushback

👉 how to respond within IRM framework

We:

- Responded with documentation — not argument

- Maintained consistency across all filings

- Framed everything within IRS evaluation logic

👉 No contradictions = smoother approval path

📊 Final Outcome

- IRS Debt: ~$140,000

- Settlement: ~$4,000

😌 What Changed

- Full compliance restored

- No more uncertainty

- No more fear of the unknown

👉 He sleeps at night

💬 “He was thorough… patient… worth every dollar… and then some.”

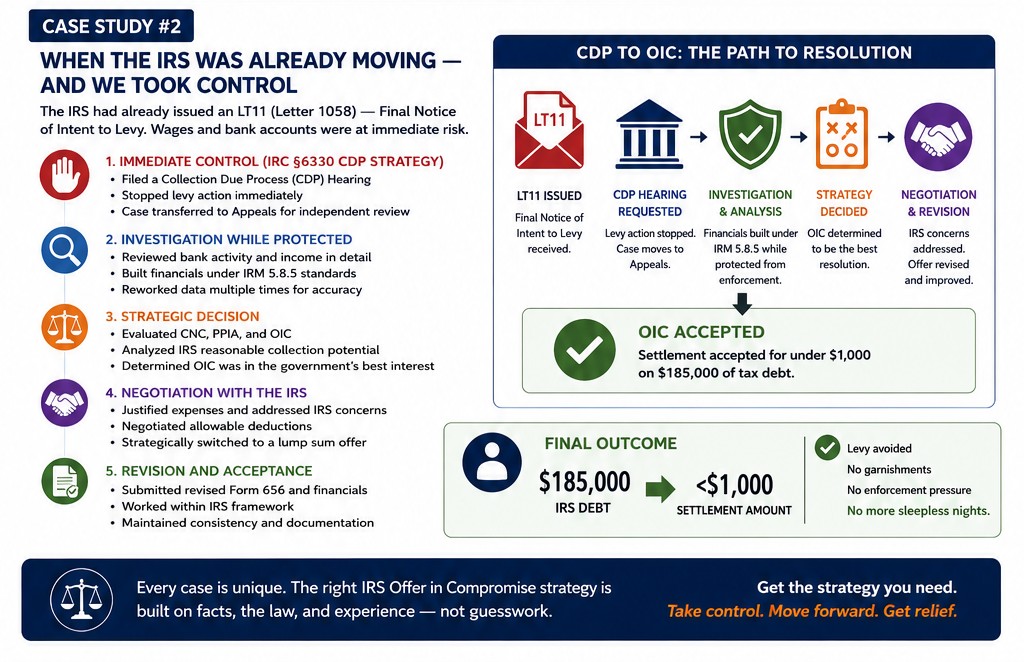

💥 Case Study #2: When the IRS Was Already Moving — And We Took Control

This case didn’t start early.

It started under pressure.

The IRS had already issued:

👉 LT11 (Letter 1058) — Final Notice of Intent to Levy

😰 What That Feels Like

At this point, it’s no longer theoretical.

It’s immediate.

👉 wages can be garnished

👉 bank accounts can be levied

👉 assets can be seized

For many taxpayers, this is where panic sets in. If you’ve received a letter like this, you already know—it doesn’t feel like a warning. It feels like a countdown.

🛑 Phase 1 — Immediate Control (IRC §6330 CDP Strategy)

We filed a Collection Due Process Hearing

This was not just procedural — it was strategic.

Under IRC §6330 and §6331(k):

- Levy action is STOPPED

- Case moves to Appeals (independent review)

- Tax Court rights are preserved

- Collection activity is suspended

👉 This gave us TIME

👉 And more importantly — LEVERAGE

It also allowed me to move the case out of the collection division and into Appeals, where resolution is evaluated independently and more strategically.

🔬 Phase 2 — Investigation While Protected

With enforcement paused, we didn’t rush.

We:

- Reviewed detailed bank activity

- Identified income inconsistencies

- Built financials under IRM 5.8.5 standards

- Reworked data multiple times to ensure accuracy

At one point:

👉 CNC was viable

But again — we didn’t settle for first option

⚖️ Phase 3 — Strategic Decision (Government Interest Analysis)

We evaluated:

- IRS reasonable collection potential

- Long-term recovery vs settlement

- Whether OIC was in the government’s best interest

👉 That is the actual legal standard under IRC §7122

We determined:

👉 OIC provided the best structured outcome

🏛 Phase 4 — Negotiation (Where Experience Shows)

This is where the case was truly won.

The IRS examiner:

- Questioned financial items

- Requested adjustments

- Reviewed medical expenses

- Evaluated offer structure

I:

- Communicated directly using IRS terminology

- Justified adjustments under IRM provisions

- Negotiated allowable expenses

- Requested structural changes to the offer

👉 Including switching to lump sum vs periodic (strategic move under RCP rules)

🔁 Revision Phase (Critical — Most Fail Here)

We didn’t resist the IRS.

We worked WITH the framework.

We:

- Submitted revised Form 656

- Adjusted financials strategically

- Maintained full consistency

👉 Stayed ahead of review instead of reacting

📊 Final Outcome

- IRS Debt: ~$185,000

- Settlement: Under $1,000

😌 What Changed

- Levy avoided

- No garnishments

- No enforcement pressure

👉 No more sleepless nights

👉 Financial life stabilized

💥 What These Cases Prove

Different facts.

Different strategies.

Same foundation:

👉 Investigation

👉 Strategy

👉 Execution

💥 Final Thought

An Offer in Compromise is not a shortcut.

It is not a guess.

It is not a form.

👉 It is something that must be built correctly

A successful IRS Offer in Compromise strategy starts with understanding your full financial picture and evaluating all available resolution options—not just submitting a form.

👉 Not every taxpayer qualifies for an Offer in Compromise—and that’s exactly why strategy matters.

📞 Take Control of Your IRS Situation

Learn more about Harmon Tax Resolution, LLC and how we approach IRS cases differently.

Harmon Tax Resolution, LLC

Will Harmon, Attorney, CPA, EA, MBA, CTRS

📍 Jacksonville, Florida (by appointment only) – 904-616-8256

📍 Port Saint Lucie Office – 772-418-0949

📍 Clearwater (satellite office) – 813-325-6009

Whether you are in Jacksonville, Port Saint Lucie, Clearwater, or anywhere in Florida, having the right IRS strategy in place can make all the difference in resolving your tax situation.

If you’re dealing with IRS debt, uncertainty, or enforcement pressure, the worst thing you can do is wait and hope it resolves itself.

The right IRS Offer in Compromise strategy can stop collections, protect your assets, and give you a clear path forward—but it has to be done correctly.

👉 Schedule a consultation today and take control of your situation before the IRS takes control for you.

❓ Frequently Asked Questions

What is an IRS Offer in Compromise strategy?

An IRS Offer in Compromise strategy is a structured approach to settling tax debt based on financial analysis, IRS rules, and the taxpayer’s ability to pay.

Who qualifies for an Offer in Compromise?

Taxpayers who cannot fully pay their tax debt or meet hardship or fairness criteria may qualify depending on their financial situation.

Can an Offer in Compromise stop IRS collections?

Yes, when properly timed, an Offer in Compromise may pause IRS collection activity and help prevent levies or garnishments.

Is an Offer in Compromise always the best option?

No, in some cases installment agreements or currently not collectible status may be better solutions depending on the facts.

Our Offices

Port St. Lucie, FL 34953

Clearwater, FL 33767

Ste#800

Jacksonville, FL 32207